.webp)

.webp)

.webp)

DALLAS — Airline privatization is often seen as just selling a national carrier from the government to private investors, but it's much more complex. It involves restructuring assets, liabilities, regulatory rights, political risks, and long-term operations.

Governments rarely sell airlines in their original state; instead, they adjust balance sheets, isolate debt, and redefine ownership to attract investors. Buyers do more than just acquire aircraft and brands; they take on operational risks, labor costs, regulatory oversight, and market volatility.

Recent debates about Pakistan International Airlines (PK) have shed light on how such deals are structured, what makes them unusual, and what investors truly gain.

Why Governments Privatize Airlines

Governments often privatize airlines because they face ongoing financial losses, rising public debt, or pressure from international lenders due to fiscal conditions. Safety or regulatory issues that require capital investment, as well as market liberalization that reveals inefficiencies, also drive privatization. Instead of focusing on maximizing sale price, governments typically privatize to prevent financial leakage and transfer operational risk out of the public sector.

What Is Actually Sold in an Airline Privatization

Contrary to what the public outside the airline industry commonly believes, buyers generally assume none of the former airline's prior debts or unfunded liabilities in the vast majority of privatizations that actually take place. There is typically just the "operating entity." Typically Included in a Sale:

- Operating certificate (AOC)

- Aircraft leases or owned aircraft

- Traffic Rights and Airport Slots

- Brand, trademarks, and goodwill

- Trained workforce and operational systems

Typically Excluded or Restructured:

- Legacy debt and sovereign guarantees

- Pension obligations

- Legal Claims and Historical Losses

- Non-core real estate or subsidiaries

Such a separation is important for attracting capital and is nevertheless misunderstood by the public as “selling cheaply.”

The Role of Pre-Privatization Restructuring

Governments almost always restructure an airline before offering it for sale. This may include transferring long-term liabilities into a separate state entity, downsizing the workforce, renegotiating aircraft leases, or restoring regulatory credibility.

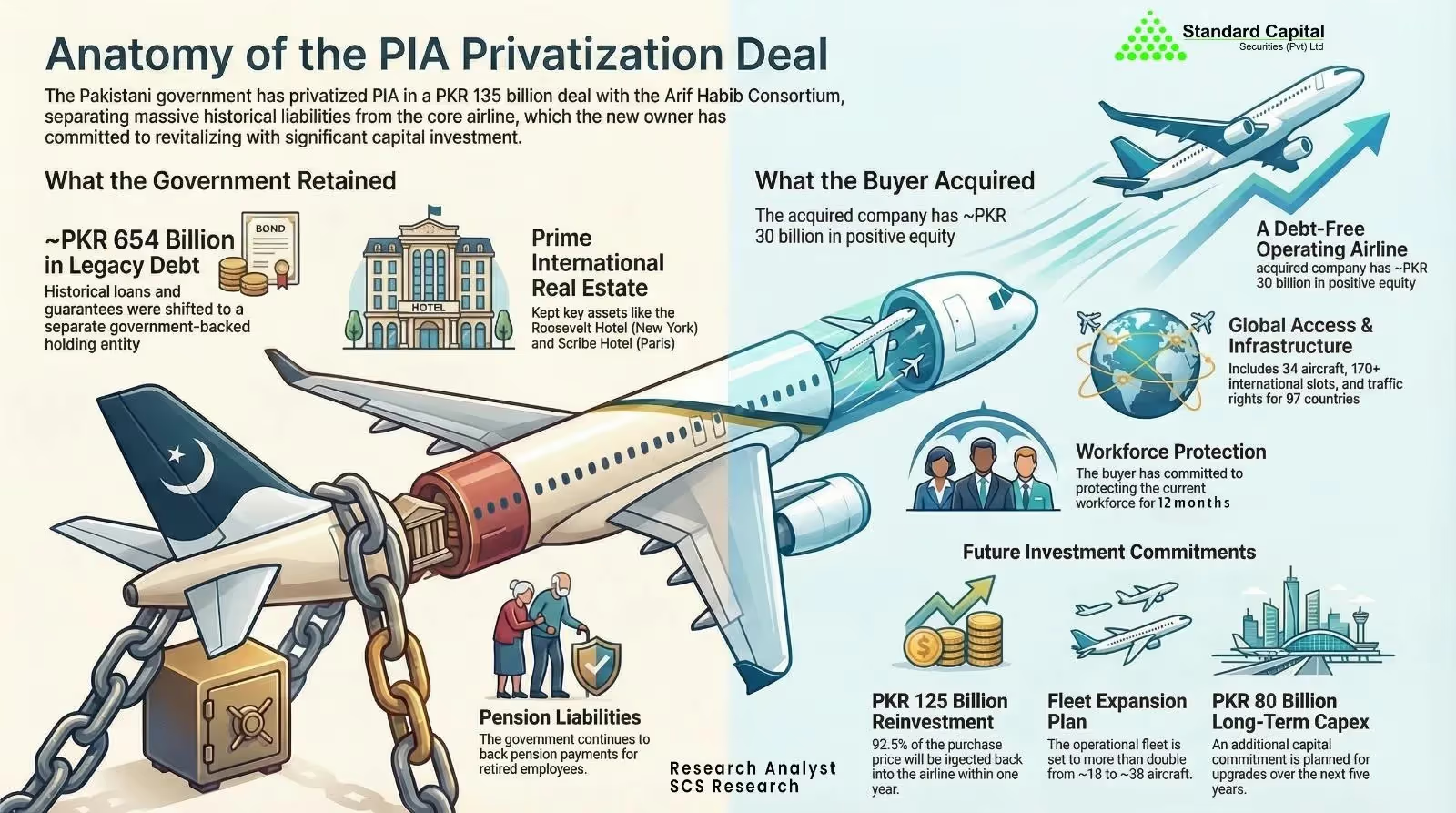

In PK’s case, billions of dollars in accumulated liabilities were shifted away from the operating airline before bidding. Without this step, the carrier would have been commercially unviable regardless of the sale price.

Such restructuring does not eliminate public costs; it merely reassigns them. The political debate often centers on this distinction.

What Buyers Are Really Paying for?

Investors value airlines not only by fleet size but by future cash-flow potential. Traffic rights, airport slots, and market access often outweigh physical assets.

Key value drivers include:

- Bilateral traffic rights

- Slot portfolios at constrained airports

- Market share in protected domestic routes

- Regulatory rehabilitation after bans or sanctions

Aircraft themselves depreciate rapidly. Rights and access, by contrast, can generate long-term returns if supported by capital and management discipline.

Ownership Structures, Control Mechanisms

Privatized airlines are rarely sold outright in a single step. Governments often retain minority stakes, golden shares, or veto rights over strategic decisions, such as route closures or changes in foreign ownership.

Table 1: Common Airline Privatization Structures

These structures reflect political sensitivity rather than commercial preference.

How Airline Privatization Plays Out in Practice

Pakistan International Airlines (PK)

The move to privatize PK illustrates how a government can prioritize reducing future liabilities over achieving a high sale price. Here, the stake sold in the deal constituted a majority of the company, while most of it found a direct route back to the company, as it was invested to improve stability by eliminating areas of major debt in the company’s structure.

The deal from a business perspective can be seen as a positive move, as the acquiring company was able to take over an already running company, along with valuable traffic rights, in addition to realizing a lower liability burden.

Additionally, part of the deal entailed the acquiring firm gaining an additional right to take over the company in full at a later time. Some of the public uproar regarding this deal can be seen as a result of perception rather than actual issues in the deal structure itself.

Kenya Airways (KQ)

An earlier model of partial privatization can be seen in Kenya Airways, which occurred in the 1990s after the arrival of a foreign strategic investor. Such a model had positive effects on the adoption of professionalism in management practices, the expansion of the airline’s route network, and integration into global airline alliances.

The periods of government interference within the company, as well as external environmental factors, indicate that a mere process of privatization may not be a yardstick for a company’s future success.

Labor, Politics, Public Resistance

Some of the strongest opposition to airline privatization often comes from employee unions, as it directly impacts job security, seniority, and pension rights. Governments must carefully balance protecting workers with maintaining operational viability, often using voluntary separation schemes or phased restructuring to do so. Political resistance typically arises when:

- Sale proceeds appear low.

- Military or government-linked organizations are involved.

- Transparency is questioned

These reactions have been observed across multiple countries and are not unique to any one nation.

Why Some Privatizations Fail

Not all airlines achieve success after privatization. Reasons for failure include:

- Continued political interference

- Insufficient capital injected

- Weak regulation

- Poor Partner Selection

Privatization transfers risk but does not reduce it in any substantive way - fuel costs, currency risks, and demand risks will all still exist in an airline business.

What Privatization Does Not Mean

Privatization does not imply:

- Guaranteed profitability

- Immediate service improvement

- Withdrawal of state influence

- Elimination of public scrutiny

Instead, it changes who absorbs losses, who makes decisions, and who answers to financial markets rather than ministries.

Conclusion

Airline privatization involves more than just selling aircraft; it mainly shifts risk, responsibility, and capital. Buyers acquire operating rights, market access, and future growth potential, while governments seek financial relief and operational stability. The controversy usually arises from public attachment to national symbols rather than airline economics.

As global aviation faces rising costs and tighter regulations, privatization remains a key strategy for governments to keep national carriers running without relying heavily on taxpayer money.

Featured image: Casey Groulx/Airways

.avif)